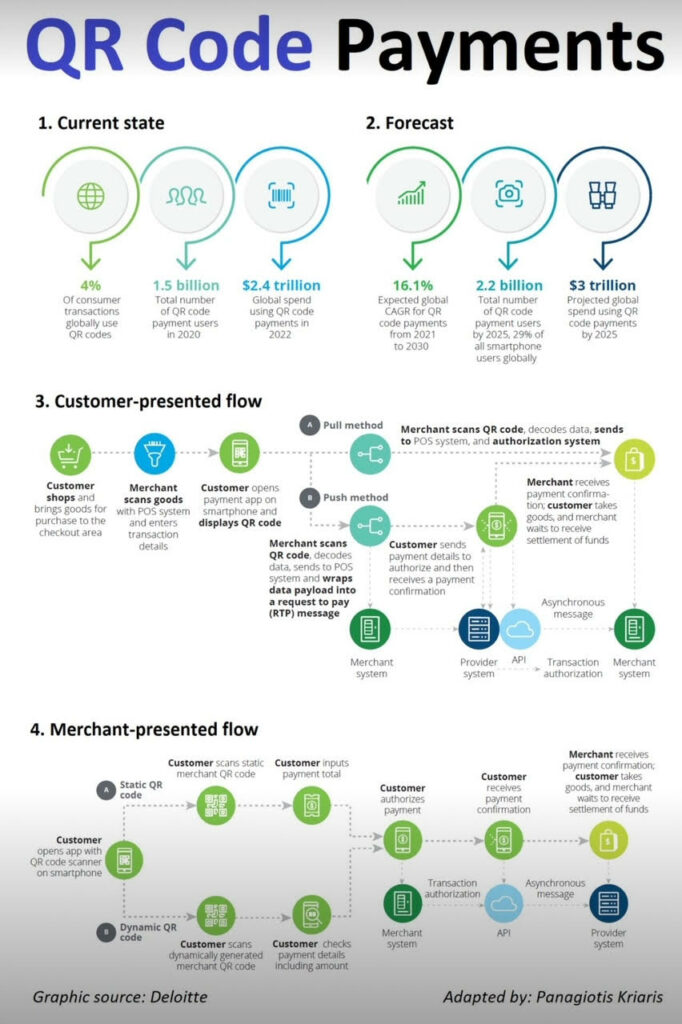

We are delighted to find individuals and organisations who truly understand the benefits of using QR Codes to trigger many customer experiences, from loading websites to executing payments between consumer and merchant. Zapper has been doing the latter since its inception in 2013, and its popularity rose significantly in the early years when the novelty factor trumped all else. Today there are many worthy competitors to the “scan-and-pay” experience, such as tap-and-pay from a multitude of devices (NFC bracelet, watch and phone, and the “old fashioned” card) and the war over convenience wages in stores, both on the high street and online every day.

The question that we grapple with continuously is: why has there been such universal adoption of QR Code payments in China while the rest of the world plays catch-up? The credit goes to WeChat Pay and AliPay who account for an extraordinarily large percentage of payments in the country (> 90%), but still doesn’t explain the origins of the “why”.

What is apparent is that the action of making a payment is usually the result of some other lifestyle action, such as shopping, dining out, paying staff and service providers, or simply paying for your parking. In the case of WeChat and AliPay, their choice was to provide access to as many useful lifestyle actions as possible to provide insanely convenient experiences to its users. I refer to this as “shifting left,” going right to the start of the customer journey and thereafter owning the end-to-end experience. Uber does this incredibly well.

Those payment providers that wish to remain in the “commodity zone,” where the race to the bottom means scale is essential, can and do offer their services in the checkout experience that all online and app vendors require. The choice remains a strategy decision.

As the Chinese super apps grew to become essential to everyday life in China, they were able to demonstrate and “enforce” the convenience of QR Code payments in the P2P experience, as well as the P2M experience. In Kenya, a unique set of circumstances gave rise to the popularity of mPesa, but USSD and short codes were the technologies used to drive the success off a massive base of feature phones. This could not be replicated in our home country, South Africa.

Zapper remains loyal to the cause of driving the adoption of QR Codes for the convenience of customers and merchants. We do not offer card acquiring machines to our merchants, and recognise that tap vs. scan is a contextual decision for the consumer, and both will remain equally relevant in the future. So why are we so bullish on the future success as the growth of QR Codes for payments is steady albeit unspectacular right now?

Convenience: Scanning a QR Code with the native phone camera launches the user into the digital experience with a single tap. The alternative would be multiple taps, and while this may seem trivial, when you consider the context that can be added, that the user does not need to know or, worse, enter themselves, the efficiency of QR Code is orders of magnitude better than any alternative. In the Zapper world, the merchant details, amount to pay, and discounts are all applied in milliseconds, which requires the user to merely confirm the transaction. Stop and think about the user control right there – the alternative is the merchant. Thereafter, any additional merchant rewards can be applied without having to present a second piece of plastic that we are all conditioned to carry around.

Dialogue: QR Code payments establish a connection between customer and merchant which cannot be replicated by tap-and-pay. Any merchant that values the new oil of the 4th Industrial Revolution, data, will choose QR Code payments to acquire access to customer data. In the high street stores, a “tap” is anonymous, whereas a “scan” is not. Merchants are able to communicate with customers and start a dialogue – how was my service? Not great this time? Please accept a voucher to return and offer us another opportunity. Merchants can assess the frequency and value of their customers before deciding how to respond to feedback on poor service.

Security: Customers don’t need to part with their payment details or have them skimmed from their physical wallets. Security of payment instruments is of paramount importance to customers, and the continuous attacks to acquire this information is relentless. While fraud detected by issuing banks is impressive, the inconvenience of replacing a compromised card is best avoided. QR Code payments (in the case of Zapper) are executed with only the consumer and the bank knowing the payment instrument details. From a merchant security perspective, we have had many scenarios in South Africa where invoices are modified to change banking details to redirect funds to the wrong (fraudster’s) account. QR Code payments don’t only protect the consumer, but protect the merchant as well from these scenarios.

No Alternative: There are scenarios where “tap” can never work – paying a bill or even a parking ticket, where paper or a digital invoice (request for payment) is received. The QR Code payment (or associated link) provides the ultimate convenience to the customer while also protecting the merchant from needing to publish their banking account details. In the case of a parking ticket, the alternative is to queue at a pay station to pay with cash or a tap. But why bother when you can skip the queue and pay on the way to your motor vehicle.

Digitisation: QR Codes can also be used for digitising processes beyond the payment. An example would be purchasing an entry ticket to an event by scanning a QR Code. The result of the payment would be to issue a digital ticket which represents the value paid for a specific event, and the scan of another QR Code at the event can be used to redeem the ticket. The entire process is digital, which does away with the need for the traditional cardboard ticket.

At Zapper, while we support all forms of payment experiences, including tap-and-pay, we think QR Codes are the coolest and most underrated payment types available today. We will continue to carry the banner to promote greater use of QR Codes in the industry and lead the way by providing innovative customer experiences that wow customers while providing all the benefits mentioned above. Our preference has always been the merchant-presented QR Code which lends itself to a better customer experience and removes the requirement for merchants to purchase hardware and ensure this remains functional.

In addition, when the customer scans the QR code, the customer remains in control of the payment experience and, amongst other things, can split a bill and add a tip, or decide which payment rails to use. The transaction remains visible on the customer’s device at all times, and with a digital wallet, can decide which card or payment type to use for the specific transaction – business expenses use the business card, while personal expenses use the bank EFT payment rails. There has been discussion in SA about standardising the QR Code which means there will be winners and losers in the process.

We don’t believe in standardisation, but certainly encourage interoperability based on commercial realities that will naturally be established between operators in the industry. Zapper has the largest interoperable network with an estimated 15 million (maybe more) consumers that are able to scan the Zapper QR Code to initiate a payment. These partners include banks and mobile money operators amongst a number of other Fintech players in the SA market. We hope by increasing the size of the network we will have many players in the industry promoting the use of the QR code as enthusiastically as ourselves.

Long may the odd array of black and white squares live and continue to bring immense convenience to all of our extremely busy lives!

To submit a release, contact us here.

{kind=link}